Market Update – July 10 – US CPI dominates this week.

With the jobs report out of the way, attention turns to CPI and Fedspeak. Today, Asian markets traded mixed, with China’s economy remaining in focus. Factory prices fell more than anticipated and CPI was also weaker than expected, adding to signs that China is seeing excess supply. China’s factory-gate prices fell at the fastest pace in 7 1/2 years in June, while CPI was at its slowest since 2021, adding to the case for policymakers to use more stimulus to revive sluggish demand as China slides to the brink of deflation. Meanwhile, at a conference in France, BOE Bailey rejected calls for setting inflation target higher than 2%.

Review of NFP: The 209k rise in nonfarm payrolls severely underperformed the whisper number (around 290) that was bloated by the massive 497k surge in private payrolls from the ADP report. That whipsawed the Treasury market that had plunged on Thursday on fears of a more aggressive stance from the FOMC. However, the overall report was decent and even stronger than expected with respect to earnings and hours worked. Fed funds futures remained priced for a July hike but trimmed expectations for a September or November move.

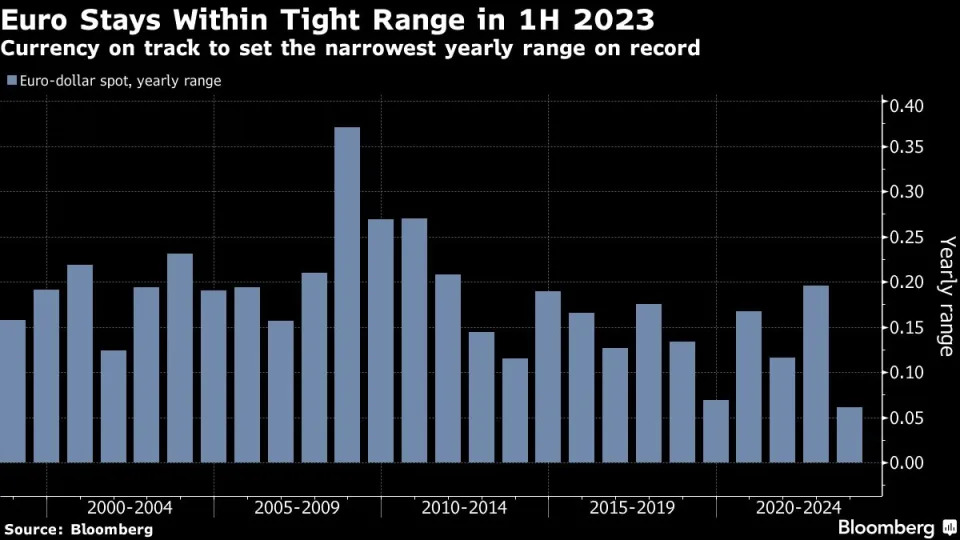

*FX – The USDIndex slumped to 101.88. USDJPY pullback to below 143 today. GBP and EUR gained ground retesting 1.2840 and 1.0690 highs, currently turning lower.

*Stocks – Hope that the official crackdown on tech companies is coming to an end, initially helped the Hang Seng and CSI300 to find buyers, but the weaker than expected data round saw indexes paring losses. Nikkei and ASX meanwhile closed with losses of -0.6% and -0.5% respectively. GER40 and UK100 futures are down -0.3% and US futures are also in the red. Alibaba (+8%) and Tencent shares today after China’s $984 million fine against the Jack Ma-founded Ant Group appeared to signal the end of the regulatory crackdown on the country’s technology sector.

*Commodities – USOil slightly lower after capping its best week since April, at $73.13.

*Gold – lower at $1923 from $1935 as traders attention turns to the US inflation. Gold had a back to back monthly loss in June.

Today – FOMC Members Mester, Bostic and Daly, German Buba President Nagel and BOE Governor Bailey speak.

Biggest FX Mover @ (06:30 GMT) LTCUSD (-1.82%) dipped to 90.195. Fast MAs flattened, MACD lines are still negatively configured with RSI at 33 and flat and Stochastic at 29 and falling.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Andria Pichidi

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.