Market News – European Stocks Higher After Another Range-Bound Session in Asia.

Asia & European Sessions:

* European stocks were poised for modest gains as investors awaited Nvidia Corp.’s earnings report for insights into the growth trajectory of AI-related stocks. Euro Stoxx 50 futures increased by 0.1%, suggesting a muted opening for European shares, while US stock futures remained steady during Asian trading.

* Asian equities fluctuated within narrow ranges due to weak corporate earnings in China.

* Hong Kong dropped as much as 1.6%, while mainland stocks fell to their lowest levels since early February. Shares of Nongfu Spring Co., a bottled water manufacturer, plummeted by up to 13% as in China sectors like materials, tech, construction, automotive, and others face significant downside risks.

* Nvidia is expected to report Q2 adjusted earnings of 65 cents per share on $28.74 billion in revenue, more than double what it earned in the same quarter last year, according to FactSet. Nvidia’s revenue has tripled annually over the past three quarters, driven primarily by the data center business. Demand for generative AI products, which can generate documents, create images, and serve as personal assistants, has significantly boosted sales of Nvidia’s specialized chips over the past year. However, Wall Street is keen on signs of any slowdown in AI demand.

Financial Markets Performance:

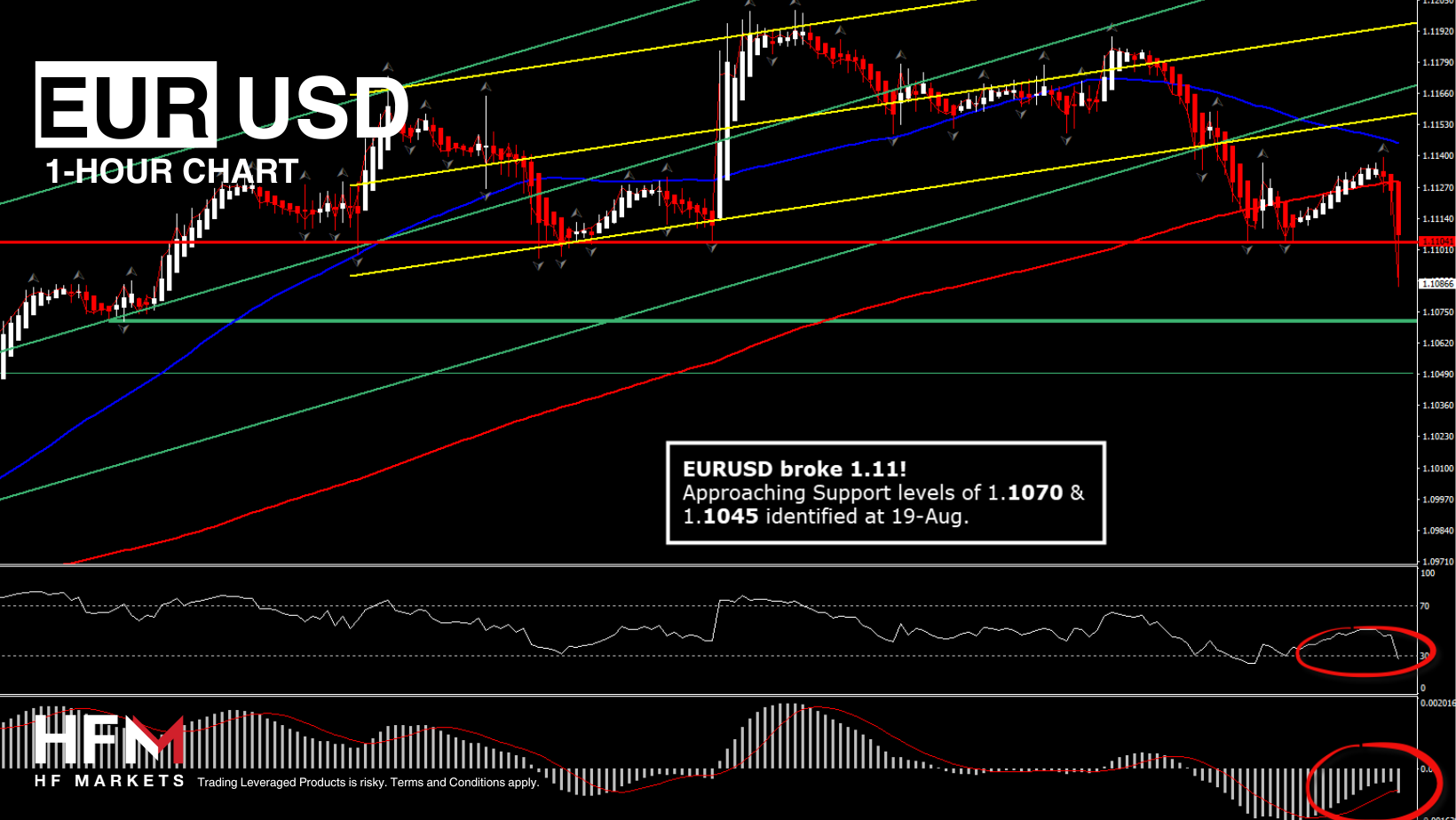

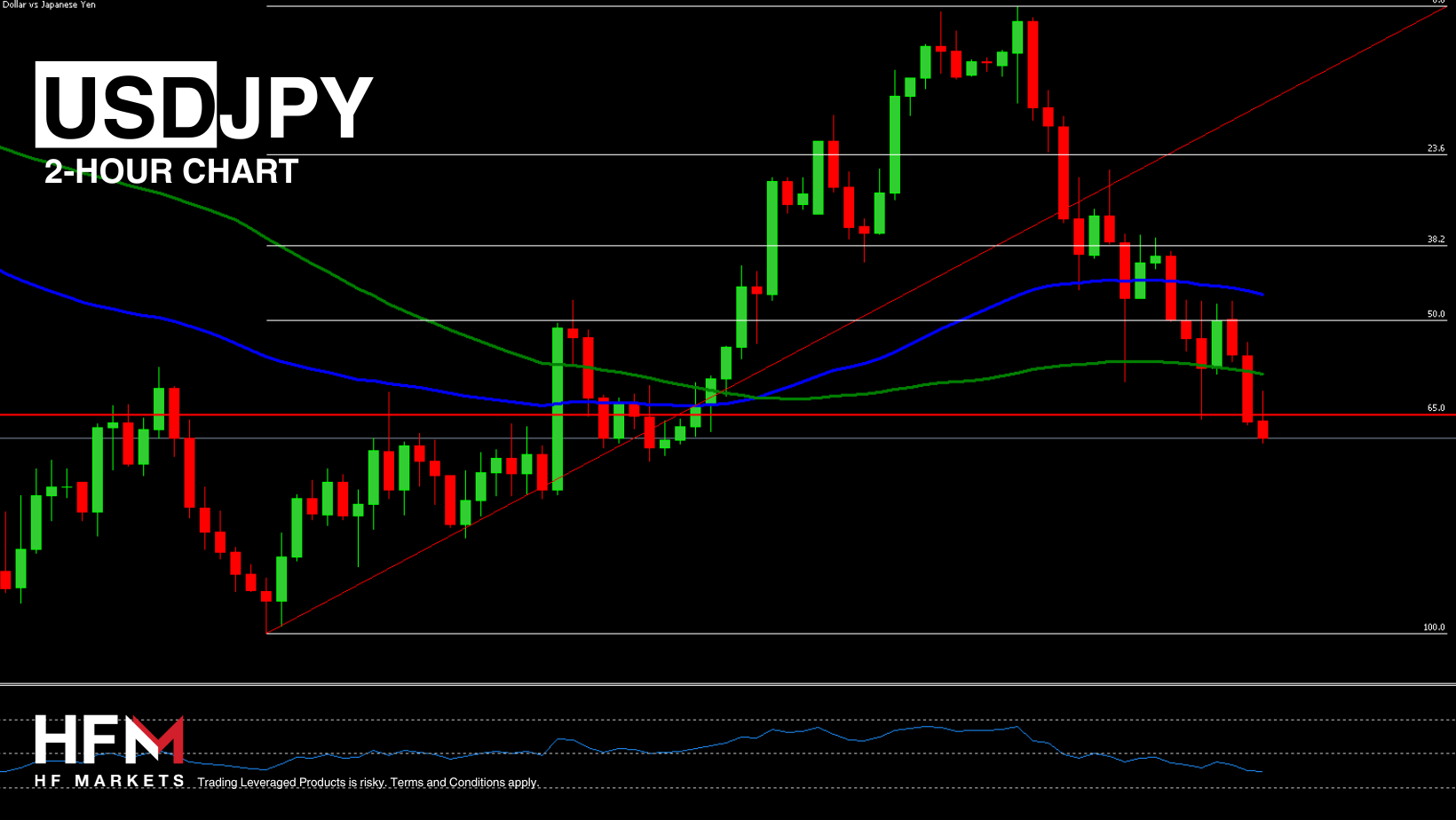

* The Yen extended its losses against the US Dollar, to 144.595 following comments from Bank of Japan’s Deputy Governor Ryozo Himino. Himino stated that the BOJ would raise interest rates as long as inflation aligns with the bank’s outlook and emphasized the need for close monitoring of developments.

* Bitcoin fell below $60,000 as part of a broader cryptocurrency market decline, including a sharp drop in Ether, the second-largest cryptocurrency.

USOil rem* ained steady after a previous session’s decline, ending a 3-day rally. USOIL is under $75. The API projected that nationwide inventories fell by 3.4 million barrels last week, which would mark the 8th decline in nine weeks if confirmed by official data later today. Crude oil has experienced volatility in recent sessions, with recent declines following a rally near the 200-DMA. Political risks in the Middle East and potential supply disruptions from Libya have supported recent gains, but a broadly bearish outlook has led major Wall Street banks like Goldman Sachs and Morgan Stanley to lower their price forecasts for next year.

* Gold retreated after a 3-day climb that brought it closer to its all-time high.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Andria Pichidi

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.